The case for investing in your Bitcoin Credit Score

First off, there is no such thing as a Bitcoin credit score or Bitcoin credit score investing…yet. Cryptocurrency is just growing out of its infancy and still has a long way to go before there is a universal credit score in the Bitcoin finance industry. However, as fast as cryptocurrency adoption is growing, it will likely come faster than we think. That is why investing in it now is such a good investment.

It is not unreasonable to think that in the future there will be an easy to reference, global “credit score” of sorts. But, I doubt it will much resemble your centralized and regulated credit score of today. In the age of decentralization with (P2P) peer to peer money and (P2P) peer to peer businesses, I am going to guess your credit score will also be (P2P) peer to peer and decentralized taking inputs from multiple (P2P) peer to peer ecosystems. So investing in a (P2P) peer to peer Bitcoin lending reputation now seems like a very safe bet towards increasing your future Bitcoin credit score.

Why do you need a Bitcoin Credit Score?

Anyone in a business understands that access to capital is an absolute necessity for growing a business or taking advantage of an opportunity. It’s important in an individual’s personal life as well. Access to affordable financing makes it possible to enjoy the finer things in life such as home ownership, a nice car, and college tuition without selling all your liquid assets.

So we can all likely agree credit is important, but you might still be asking the question of why you need a “Bitcoin” credit score. The answer is because if you’re reading this, you likely already understand that finance and money are moving onto the blockchain whether you like it or not. And you also likely understand that the fiat fractional reserve finance system doesn’t work on the blockchain with sound cryptocurrency money. And if the current finance system doesn’t work, neither will your current financial reputation or credit score.

Without going into too much detail, Bitcoin will kill banks, not banking or finance. It will just make it much different. I may be a little bit advanced in my prediction that fiat banking and finance gets completely kicked to the curb, but an investment in your Bitcoin reputation now can give you a jumpstart in the coming blockchain decentralized economy.

Financial Reputation as an investment

First I want to solidify that reputation is an investment, even if we don’t normally think of it that way. For example, when I was young I took out 3, $1000 collateralized loans at my local bank to create a credit history and begin building a positive credit score. I had no need for the money, but I knew I wanted to invest in real estate later and a high credit score would become very valuable in the future. So I invested the time, energy, and interest payments into building my financial reputation or credit score. Which I think can be directly compared to investing the time, energy, and finances investing in stocks, bonds or other asset classes.

Later after the real estate collapse, I was able to leverage the investment I made in my credit score to obtain financing and purchase a very cheap rental property (which through rent has returned 40% APR for 7 straight years). In short, building a solid credit history is an investment for future opportunities or savings on loans (because of lower interest rates).

The Investment

There are 3 good reasons why investing in your Bitcoin Credit Score is a good investment.

- Hedge for fiat disruption

- Length of Credit History

- Real Market interest rates

1. Hedge for Fiat disruption

If you are well established in the fiat world and have a really good credit score, history, and access to capital. Investing in your Cryptocurrency based reputation now is a good hedge towards losing all of that in a fiat collapse. And even if fiat doesn’t collapse, and the current financial system slowly moves into cryptocurrency, your investment will still be worth at least what you put into it, if not more.

Having been involved with Peer to Peer P2P Bitcoin lending for the last 2 years, I can tell you now that your credit score and fiat reputation will not transfer well into the crypto finance industry. They are currently like oil and water which doesn’t mix. So don’t expect it to, and start building a crypto lending reputation before you need it.

2. Length of Credit History

Just like in the fiat world, length of credit history is a very important and heavily weighted input in deciding the creditworthiness of someone. The fact of the matter is that new borrowers are risky. This risk cannot really ever be avoided but, it can be done on a very small low risk scale at first and built up over time. For example when I turned 18, I opened up a small credit card I didn’t really need and paid it back every month. After 3 years of paying back a credit card and using the limit modestly, that credit card issuer now has good information and history to increase the credit issued to me based off my good history.

It’s no different in the cryptocurrency world, but it’s more important as institutions like the US credit score system don’t yet exist. So even if you don’t need to borrow Bitcoin or other cryptocurrencies now, it’s not a bad idea to open a small crypto credit line and start slowly building a nice cheap low risk history.

3. Real Market Interest Rates

Today’s environment for lending is fantastic. Interest is cheap and money is loose! You can finance almost anything, and with such low interest rates it makes sense to do it. Why wait for tomorrow what you can borrow and have today?!

Unfortunately the whole fiat market is fraudulent, and the current central bank interest rates are extremely manipulated and not anywhere near the real market interest rates.

In cryptocurrency, the market decides interest rates and they are much higher than fiat interest rates. Because cryptocurrency is sound money and cannot be created out of thin air like at banks, the supply of cheap loans is very low. And supply dictates the market, as we know there will always be plenty of demand for cheap credit.

In my experience even on low risk collateralized debt, the real interest rate is going to be over 10%. So if in the future you need to finance your home purchased with cryptocurrency, you can likely expect an interest rate of at a very minimum, 15% (more likely 20-30% for a high leverage long-term mortgage). So, building a better Bitcoin credit score now while you don’t need it can pay huge dividends getting a lower interest rates in the future when you do need it.

Why Digital Identity is Different

Having established the value of a financial reputation in the cryptocurrency world, now comes the trickier part of building digital identity to attach that reputation to.

Digital identity is currently different than our more tangible and established government identity. This is important because it is still possible for people to exist completely out of the digital world. A person can for example default and destroy their online identity defaulting on a Bitcoin loan, and then just simply not go online anymore (or go online anonymously) and be no different for it. They could still go to the bank and get a loan, open a credit card, and most everything else financially. This is because a default on a Bitcoin loan does not yet easily affect your fiat based credit score or reputation. And until that is not the case, a digital identity with reputation needs to be built.

When Online reputation works

Like or dislike the Silk Road dark web exchange, its usefulness as an economic experiment is valuable. The silk road taught us that trust can exist in a completely trustless environment. At the time, Bitcoin was almost completely anonymous and most users were completely anonymous doing sometimes illegal transactions. But, millions of dollars worth of free trade happened using nothing but online reputation in a forced rating system.

Ebay is a much more common and well known rating system. Reviews and ratings align the incentives for the seller to give the best service possible. And the positive feedback loop of highly rated sellers getting more business only makes the system stronger and the service better. There is also a negative feedback loop as those who get bad reviews get less business, and eventually go out of business.

When Online reputation Doesn’t Work

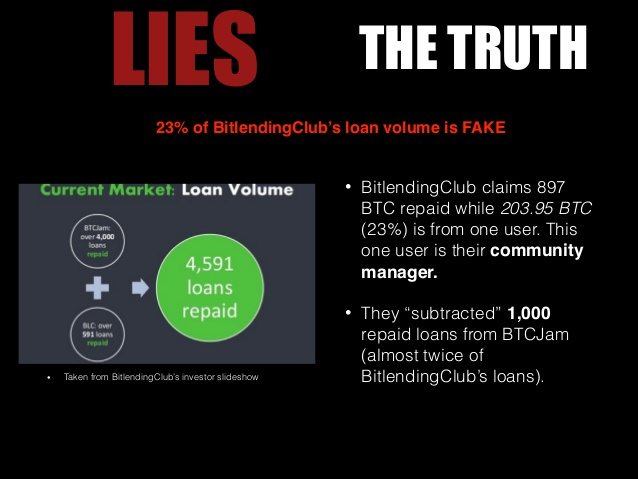

A case for online reputation not working is early Peer to Peer Bitcoin lending at Btcjam. People had to register and verify their identity with Btcjam, however, Btcjam’s verification process was not very thorough. They also could attach other reputation based online identities such as Twitter, Facebook, LinkedIn, and Ebay accounts. But, when the time came to pay back Bitcoin loans after the price went up 40%, Peer to Peer lending learned something important. Online identity is not yet that valuable. Bitcoin borrowers very quickly decided that they valued their online reputation much less than the extra money due for their loan because of the Bitcoin price increasing. So defaults went through the roof, and borrowers didn’t really suffer credit consequences for their theft as the legal system for Bitcoin loans is not yet established.

Digital Reputation has a price, and it starts very low

Whether we realize it or not we all have a price tag for our reputation in all of its forms. The price is of course different for everyone as value is subjective. Some people would ruin their reputation over a $70 cable bill, and some would never ruin their reputation unless they absolutely had to. It’s frankly impossible to know for certain what someone values their reputation at, and if they are a good credit risk.

However, to reiterate point #2 Length of Credit History is especially important when it comes to digital identity. Because, in the digital world you can always create a new account. For example, If someone offered me $500 to ruin my Telegram reputation, an account I started 3 weeks ago, I would hand it over to them with a smile. However, if they made the same offer for my 8 year old Facebook account I would instantly reject them. This is because I have a lot more history in input that I would lose in my facebook account compared to my Telegram Account.

Where to Build your Bitcoin Credit Score

As it is such a young and developing industry there are not very many options on where to build your bitcoin credit score yet. Some good bets are Peer to Peer(P2P) companies that have been around awhile such as Btcpop.co and Bitbond.com which have both been around since 2014.

However there are a host of new lending platforms coming up such as Ethlend (decentralized lending on Ethereum). Btcloans.org will follow up with further articles on how and where to build your Bitcoin credit score.